Preparing for retirement is more complicated than ever.

People are living longer, rising inflation is threatening the buying power of retirement savings and Social Security benefits, and there’s a looming threat of Social Security cuts on the horizon. Faced with these challenges, you’ll likely want a generous nest egg to ensure a comfortable retirement.

For most people, $2 million would qualify. Saving $2 million would provide about $80,000 in retirement income (assuming you follow the 4% rule), but it’s going to require diligently investing money to hit that target.

So how could you amass $2 million? Two Motley Fool writers have outlined different paths to get you there depending on your risk tolerance and investing knowledge.

Image source: Getty Images.

Path 1: The slow but steady path

Christy Bieber: The first option to amass a $2 million retirement nest egg is to put your money into an S&P 500 index fund. There are a number of options, including:

While these ETFs differ slightly in terms of their expense ratios and exact return-on-investment, all three are designed to closely mimic the performance of the S&P 500, a financial index made up of 500 of the largest U.S. companies.

The S&P 500 has historically produced around a 10% average annual return over the long term, although of course it’s lost money in some years and done better during others. Because an S&P fund gives you exposure to 500 of the most profitable large businesses in the U.S., the risk of investing in it is minimal. And you’re very likely to earn returns close to these historic averages over time.

This approach is a simple one for those who don’t want to spend time picking individual stocks. It’s even the one Warren Buffett recommends for the majority of investors. But the downside is, you’re extremely unlikely to exceed that average 10% return by much over the long haul — which means you may need to invest a lot of money to grow a $2 million fortune.

The table below shows how much you may need to invest each month depending on when you start. It’s based on retiring at the age of 65 and earning the average 10% return you can reasonably expect the S&P to provide.

| If you start investing at | You’ll need to save this much each month to have $2 million at 65 |

|---|---|

| 25 | $376 |

| 35 | $1,013 |

| 45 | $2,909 |

| 55 | $10,457 |

When you’re limiting your potential returns to 10%, the monthly investment required may be higher than if you built a portfolio of stocks that substantially outperformed the market. Of course, you’re taking on far less risk. While you could lose a lot of money by investing in individual stocks, it’s extremely unlikely you’ll suffer big losses if you put your money into an S&P fund and leave it alone for decades.

Path 2: The golden age of individual investing

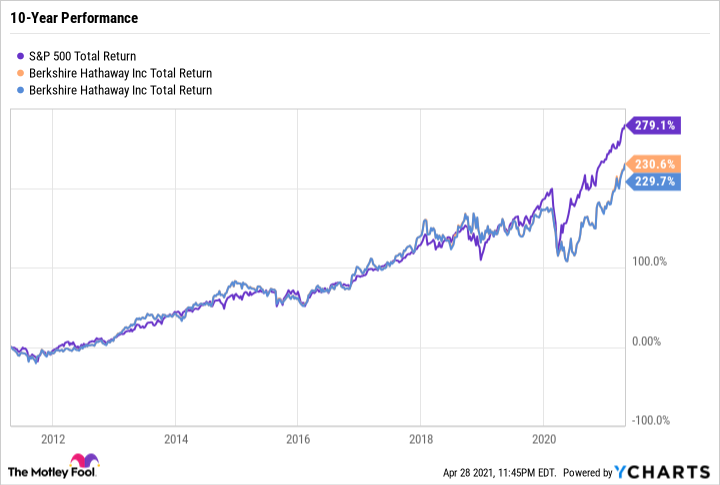

Daniel Foelber: With a little luck, anyone can beat the market over a year or two. But outperforming over the long term is a much harder feat. According to a recent S&P Indices Versus Active (SPIVA) report, just 14% of U.S. active funds and just 6% of large-cap U.S. active funds beat their benchmarks from 2001 to the end of 2020. In 2019, less than 30% of active U.S. fund managers beat the benchmark after fees. And even Warren Buffett’s Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B) has underperformed the S&P 500 over the last decade.

The data may not look good for active fund managers. But you and I aren’t active fund managers. We are individuals living in the golden age of investing.

Today’s wealth of knowledge and access to free information equals power without the once hefty price tag. The edge that Wall Street once had over Main Street has become blunt. In fact, Wall Street actually has many disadvantages. Active funds and even ETFs have to abide by rules and regulations, and adhere to the framework outlined in what’s called a prospectus. Investors in the fund may raise their eyebrows if managers over-allocate into unproven companies or face short-term volatility. This can lead to premature selling before a company has the chance to break out or there is so much diversification that the fund practically mirrors the index.

Active funds can also face outflows after a bad quarter. In sum, active funds face quite a bit of inflexibility that the individual investor simply doesn’t have to deal with.

Building a $2 million retirement nest egg over the course of a few decades can be an enjoyable process fueled by a combination of individual stocks, index funds, ETFs, fixed-income vehicles, and more. I agree with Christy that picking individual stocks can be time-consuming and even stressful. It adds a layer of ownership over your financial future that amplifies the joy of gain and the sorrow of loss. We are all human and will handle the psychological pressures of investing differently. But for those curious to learn about individual companies, allocating a portion of savings toward picking stocks can be worthwhile.

The main reason to invest in individual stocks is that there are flaws with the S&P 500. It is chock-full of losers that weigh down the performance of the winners. Although the recovery from the pandemic-induced March 2020 lows has been nothing short of remarkable, it’s really been led by just a few sectors. Many small-cap stocks with big-cap potential also aren’t included in S&P 500 index funds. Whether its growth stocks or dividend stocks, picking individual companies and letting your winners run opens the door to explosive gains simply unattainable with an index fund. And it’s easier than ever, now that many brokers offer $0 trading fees.

The market misprices securities all the time. It is governed by human emotion and therefore isn’t perfectly efficient. Peter Lynch, one of the best investors of all time, believed that regular people can beat the market by investing in businesses they understand better than Wall Street. At the Motley Fool, we want to help you understand good companies and avoid bad ones. With the right temperament and time horizon, picking individual stocks can be a great way to amass $2 million and live a long and happy retirement.

This article represents the opinion of the writer, who may disagree with the “official” recommendation position of a Motley Fool premium advisory service. We’re motley! Questioning an investing thesis — even one of our own — helps us all think critically about investing and make decisions that help us become smarter, happier, and richer.